ExtremeHurst™ is a quantitative detector of extreme investor behavior. Specifically, strong trend-persistent stock price movements are evidence of positive feedback, such as investors irrationally buying because the price is going up…which drives prices higher, etc.

In 1994, Parallax found a way to measure extremes of mean reversion and trend persistency by using multiple measurements of the Hurst exponent. We found that these extremes are unstable points in financial markets that are characterized by discrete scale invariance, accelerating price, and log-periodic cycles. At these points new trends begin and end.

We built a filter to identify these events on any time scale. See the examples on the right.

Extension Examples:

Compression Example:

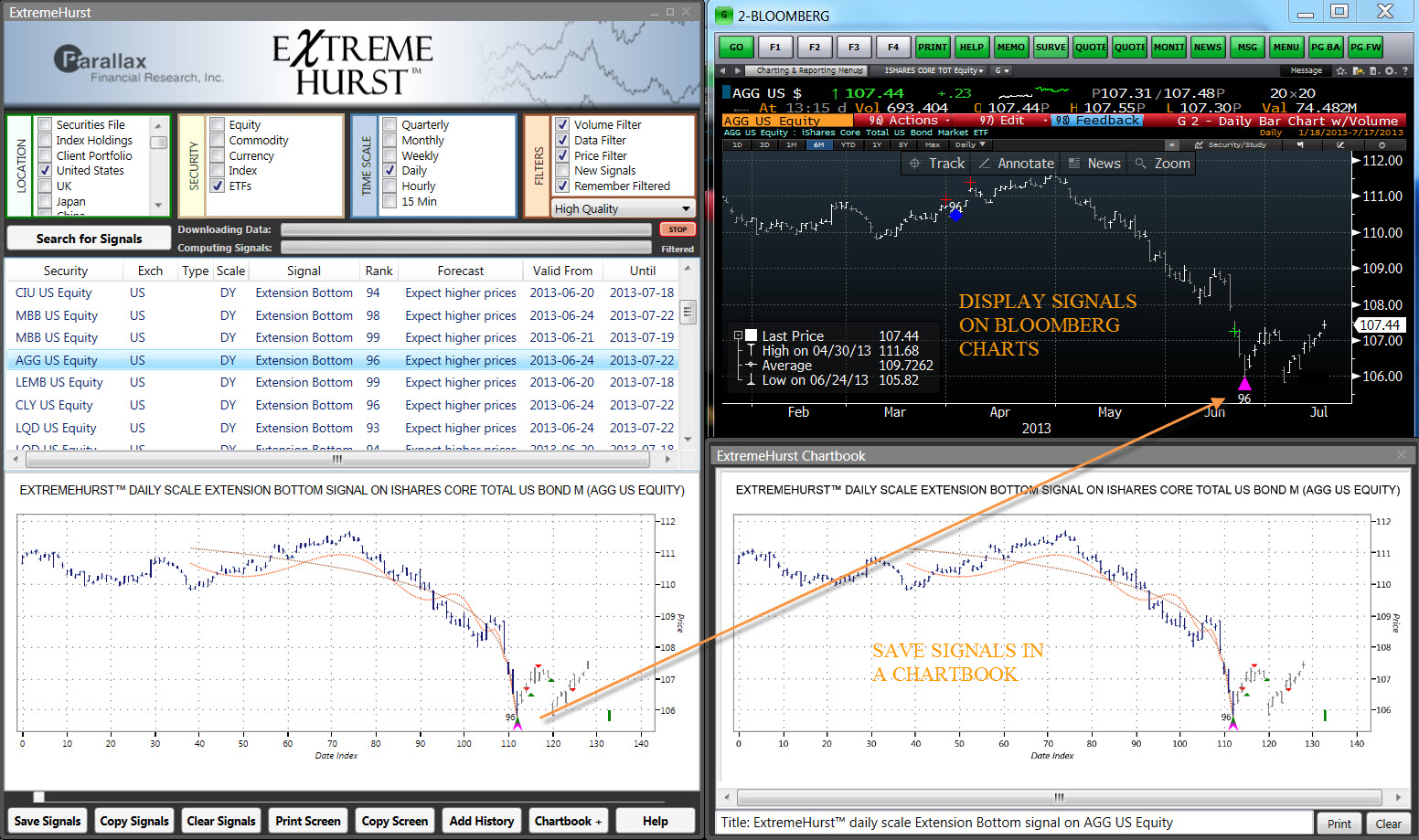

ExtremeHurst™ on Bloomberg

ExtremeHurst is on the Bloomberg Terminal in different forms and can be accessed by entering “APPS EHURST” for the scanner, “APPS CS:PFR” for G chart overlays, or “APPS PFEX” for our EXCEL add-in. The Bloomberg platform was chosen as a host for this product because of its exclusive access to worldwide financial data on all time scales, and because of its position as the leading institutional platform. For the first time ever, subscribers will be able to search the world for Extension and Compression signals! Our product is written using Microsoft’s .NET library, the C# programming language, and then linked to Bloomberg data servers through the Bloomberg API.

More Information

- ExtremeHurst User’s Guide

- ExtremeHurst Video Tutorial

- Parallax Indicators Video Tutorial

- ExtremeHurst for Bloomberg Sample Chartbook Output

- Financial Seismology: Exploiting the Hurst Exponent (ExtremeHurst is discussed)

- ExtremeHurst Hints and FAQs

- ExtremeHurst for Bloomberg Flyer

Get ExtremeHurst on Tradestation:

Parallax Market Timing Software on TradeStation

Sales & Sales Support

For Bloomberg products, contact Kris Kaufman:

phone: +1-425-868-2486

Teams: s.kris.kaufman

email: kkaufman@pfr.com

Bloomberg IB Chat at: SKAUFMAN

The users guide for this product can be found here.